Interest Payable on a Loan Becomes a Liability:

Interest is neither a liability nor an asset. Interest payable on a loan becomes a liability.

:max_bytes(150000):strip_icc()/ScreenShot2021-08-21at5.02.29PM-f5d77e3185ff4122a026ba2a6c89c6de.png)

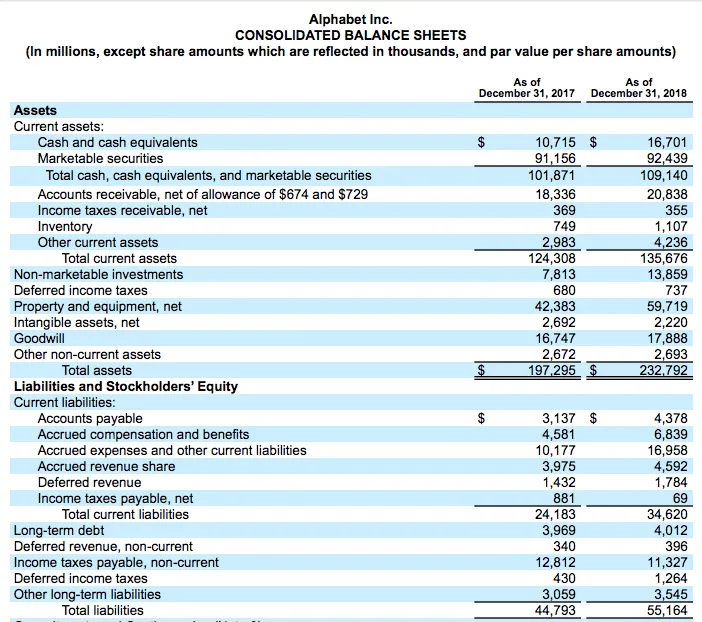

Liability Definition

Current liability account Interest Payable must report.

. It is the amount of interest a company owes to a the lenders it has borrowed any debt from or b to the lessor it has leased any capital lease from. Interest payable on a loan becomes a liability when A. On November 1 Year 1 Noble Co.

This is the amount incurred but not paid as of the date of the balance sheet. When the borrowed money is received. However if youre talking about the actual payment or.

You would include the interest for December 29 30 and 31st as an accrued liability. Payroll taxes and mandated programs such as workers compensation insurance. When the note payable is issued.

Interest Payable Interest Payable is a liability account shown on a companys balance sheet that represents the amount of interest expense that has accrued Interest expenses that have already occurred but have not been paid. When the borrowed money is received. There are several differences between the two concepts.

Debit Interest Expense 550 and credit Cash 550. Liability for loan is recognized once the amount is received from the lender. Accounting for loan payables such as bank loans involves taking account of receipt of loan re-payment of loan principal and interest expense.

The borrowed money is received. Interest payable on a loan becomes a liability. When the note payable is issued.

If any portion of the loan is still payable as of the date of a companys balance sheet the remaining balance on the loan is called a loan payable. Interest payable is a current liability. 1 answerTherefore the interest payable becomes a liability the moment the borrowed money is received.

Current Portion of Long-term Loan in case of a loan that is payable is more than one year this heading would only include the portion of loan and interest that is payable in the current 12-months. At the maturity date. Examples of Interest Expense and Interest Payable.

This current liability account reports the amount of interest the company owes as of the date of the balance sheet. But the Bank Interest is what we have to pay through the entire life of loan takeneventually it becomes an expenseHowever prepaid bank interest is a short term asset. Debit Interest Expense 550 and credit Interest Payable 550.

List the current portion of the loan payable and any accrued interest expense under the. Interest expense is calculated on. Interest payable is a current liability.

Interest payable is the amount of interest the company has incurred but has not yet paid as of the date of the balance sheet. Generally accounts payable are the largest current liability for most businesses. The remaining principal amount is reported as a long-term liability or long-term liability.

When the note payable is issued. Non-current liabilities are the liabilities that are payable after a period of 12 months. Debit Discount on Notes Payable 1100 and credit Interest Payable 1100.

Any principal amount payable within 12 months after the balance sheet date is reported as a short-term liability. Group of choices when the borrowed money is received. At the maturity date.

Interest payable on a loan becomes a liability when A. It is only recorded with the passage of time as the interest owed becomes an actual liability. Interest payable on a loan becomes a liability.

Second interest expense is recorded in the accounting records with a debit while interest payable is recorded with a credit. The interest that a borrower will owe on a loan in the future is not recorded in the accounting records. Interest payable on a loan becomes a liability.

When the note payable is issued. At the maturity date. Interest payable on a loan becomes a liability when A.

Borrowed 80000 from South Bank and signed a 12 six-month note payable all due at maturity. When you make that loan payment you pay interest up to December 28. Future interest is not reported on the balance sheet.

The interest on this loan is stated separately. An employers total payroll-related costs always exceed the wages and salaries earned by employees by. At the Interest payable on a loan becomes a liability.

Future interest is not recorded as a liability. At the maturity date. First interest expense is an expense account and so is stated on the income statement while interest payable is a liability account and so is stated on the balance sheet.

Liabilities are understated by 8333 accrued interest payable. Interest Payable is also the title of the current liability account that is used to record and report this amount. The borrowed money is received.

Any interest accrued since the last payment must be reported as Interest payable a short-term obligation. On November 1 Greenfield Corporation borrowed 55000 from a bank and signed a. On November 1 Year 1 Noble Co.

Borrowed 80000 from South Bank and signed a 12 six-month note payable all due at maturity. At that point you will be liable to pay the first. If youre paying it interest is treated as an expense.

The borrowed money is received. Interest payable on a loan becomes a liability when. Group of answer choices when the borrowed money is received.

Genarally it is an expenseIf the company is granted with a bank loan it becomes an longterm obligation for the company Therefore Bank Loan is a Liability. The interest on this. If youre receiving it interest is revenue.

A Beginner S Guide To The Types Of Liabilities On A Balance Sheet The Blueprint

Long Term Liabilities On Balance Sheet Definition List

/dotdash_Final_Current_Liabilities_Sep_2020-01-6515e265cfd34787ae2b0a30e9f1ccc8.jpg)

Current Liabilities Definition

Introduction To Balance Sheets Positive Money

Comments

Post a Comment